Industry scenario: The industry witnessed a shift in consumer preference to 14- carat/18-carat gold jewellery as well as lightweight jewellery due to spike in gold prices. This is evident from about 15% increase in ATV (avg. ticket value) to Rs 73,000 which is lesser than the rise in gold prices. The share of old gold exchange has also gone up to 39-40% of the total sales (vs. 25% 2-3 years back) owing to high gold prices. Out of this, more than 60% was from non-Senco customers which reflects healthy shift from unorganized to organized market.

Total addition of 5/16 stores in 4QFY25/FY25: The company opened 5 new stores in 4QFY25 comprising of 2 company-owned-company- operated stores (COCO) stores, 2 franchise stores and 1 FOFO store. During FY25, Senco added 16 new stores – 6 franchise stores, 9 COCO stores and 1 Sennes stores (for lab-grown diamond, perfumes, and leather bags) taking the total store count to 175 as of Mar’25.

Guidance & Outlook: Management has reiterated topline growth of 18-20% in FY26 and grow PAT with focus on improving diamond sales. The company targets EBITDA margin of 6.8-7.2% and a PAT margin of 3.5-3.7%. In a high gold price environment, management will focus on lightweight jewellery while the wedding segment contribution will continue to remain around 35-40% of the overall business. It further expects 15-20% volume growth in diamonds with shift in consumer preference towards lower-purity, lightweight and diamond studded jewellery. The company aims to add 18-20 stores in FY26 with high focus on adding more franchise stores (minimum 10 franchisees and 8-10 COCO stores) with strong focus on opening stores in East India and North India. With increasing diamond sales, the company is confident of achieving 15% stud ratio in next 3-4 years.

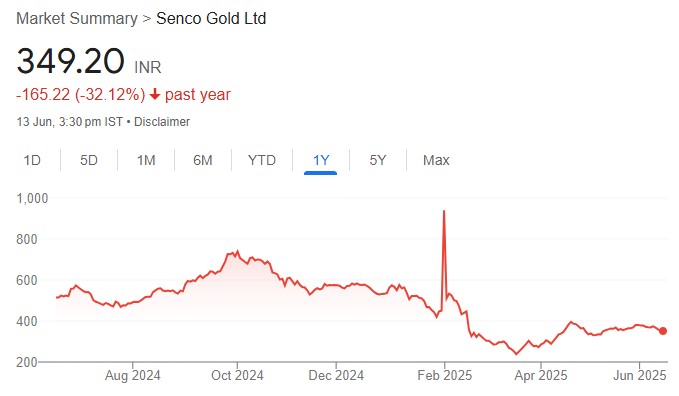

Maintain BUY – Target Price unchanged at Rs 431: We have done minor changes in our FY26E/FY27E PAT estimates factoring in the latest guidance and outlook on the company. We value the company at 32x of its 1-Yr rolling forward EPS and keep our target price unchanged at Rs 431 which implies an upside potential of 15.3% for 12-18 months.