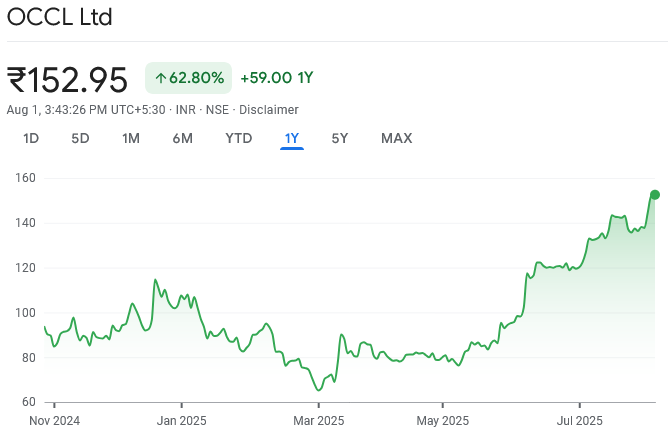

OCCL Ltd has several positive triggers. Buy for TP of ₹227 (50% upside)

Posted: Fri Aug 01, 2025 8:23 pm

OCCL reported much better performance & stronger margins than our estimates. The performance was better because of higher sulphuric acid margins & lower operational cost during the quarter. OCCL revenue grew by ~14.5% QoQ majorly led by higher insoluble sulphur & sulphuric acid realizations. YoY comparison cannot be done because of demerger adjustments. The blended utilization stood at ~75% as on Q1FY26. During the quarter, lower freight & lower other cost led to steep improvement in EBITDA margins to ~21.4% vs 17.4% in Q4FY25. The Insoluble Sulphur (IS) industry remained largely weak with soft recovery from international markets along with subdued domestic market. Going ahead we feel the global IS industry will improve gradually but current issues like oversupply situation might take at least ~1 year to normalize, although early signs of stabilization is seen. Export markets like Europe are suffering with muted demand & heightened geopolitical issues which is impacting recovery. Even in Indian market, competitive intensity had increased in H1CY26 & OCCL also lost some market share to its rivals but is now on course to improve its lost glory supported by imposition of ADD. Imposition of ADD against China & Japan will protect OCCL margins in the coming years. Also, backed by a strong foundation, operational agility and long-standing customer relationships, we remain confident in the ability of the company to emerge stronger and capture growth as the environment stabilizes. Some positive points about OCCL are its foray in North American market wherein company had already cleared trial runs & better pricing mechanism will lead to margin improvement for the next 2 years. We anticipate recovery will gradually happen over the next 2 years, although imposition of ADD has largely upgraded our PAT estimates by ~26%/~38% PAT over FY26E/27E respectively. The jump in our estimates is led by upgrade of both volumes & realizations. Since our last update, the stock has already witnessed a decent upmove, despite this the stock has more room on the upside. We upgrade our target P/E multiple to 15x (earlier 12x) to March 27E EPS of Rs 15.1 & thereby, arrive at target price of Rs 227 per share which is an upside of ~50% from the current valuations. We maintain our BUY rating on the stock.

Overcapacity a cause of concern, IS pricing improved & freight cost normalized, ADD imposition is game changer

▪ Globally oversupply situation in IS business has caused worry to global IS manufacturers as demand pace is slow & during covid times in anticipation of rising demand manufacturers build capacity faster & as demand pace faltered, the extra volumes are being dumped in global markets at cheap prices. OCCL too bears the brunt of higher dumping from China & Japan which led to poor margins in the last 2 years.

▪ However, with recent imposition of ADD, it will OCCL to offset the adverse effects of dumped imports.

▪ During the quarter, IS & sulphuric acid pricing has witnessed uptick, freight cost has normalized & other lower operational cost led to better than anticipated EBITDA margins during the quarter.

▪ Over the years, OCCL has lost market share to its rivals but with recent ADD imposition couped with enhanced product quality with dispersion & thermal stability properties, we feel company is looking to gain back its lost market share once import volumes witness dip & demand supply balance achieves.

Focussed on increasing its foray in newer geographies, tariff uncertainty remains, competitive intensity high

▪ The company is focussed on enhancing its export business by targeting geographies like North America. However, other manufacturers like Shikoku Chemicals (Japan) & China Sunshine (China) are also increasingly looking to tap North American market which will increase competitive intensity globally.

▪ Here, US tariffs also play a pivotal role to get an edge in the North American market. As of now, tariff uncertainty remains & India (25% duty) remains on the backfoot compared with Japan (15% duty) on exports to US.

Valuation

▪ We model in higher volume growth of ~7% (earlier ~5%) & higher realizations from FY25-27E. Imposition of ADD should be a game changer as it will improve the margins & ROCE of the company. Concerns around weak export market & slower industry growth remains an overhang but is transitory once global demand picks up pace. Also, IS price has witnessed improvement by 25-30% from the bottom, stabilization of raw material prices, normalization of freight cost and strong FCF generation (FCF yield of 10-15%) are the positives.

▪ Currently, the stock is trading at P/E of ~10x on March 27E EPS of Rs 15.1. With imposition of ADD & stated positive triggers, we upgrade our target multiple to 15x (earlier 12x) and arrive at a target price of Rs 227 per share which offers upside of ~50% from current valuations, thereby maintaining our BUY rating on the stock.

Overcapacity a cause of concern, IS pricing improved & freight cost normalized, ADD imposition is game changer

▪ Globally oversupply situation in IS business has caused worry to global IS manufacturers as demand pace is slow & during covid times in anticipation of rising demand manufacturers build capacity faster & as demand pace faltered, the extra volumes are being dumped in global markets at cheap prices. OCCL too bears the brunt of higher dumping from China & Japan which led to poor margins in the last 2 years.

▪ However, with recent imposition of ADD, it will OCCL to offset the adverse effects of dumped imports.

▪ During the quarter, IS & sulphuric acid pricing has witnessed uptick, freight cost has normalized & other lower operational cost led to better than anticipated EBITDA margins during the quarter.

▪ Over the years, OCCL has lost market share to its rivals but with recent ADD imposition couped with enhanced product quality with dispersion & thermal stability properties, we feel company is looking to gain back its lost market share once import volumes witness dip & demand supply balance achieves.

Focussed on increasing its foray in newer geographies, tariff uncertainty remains, competitive intensity high

▪ The company is focussed on enhancing its export business by targeting geographies like North America. However, other manufacturers like Shikoku Chemicals (Japan) & China Sunshine (China) are also increasingly looking to tap North American market which will increase competitive intensity globally.

▪ Here, US tariffs also play a pivotal role to get an edge in the North American market. As of now, tariff uncertainty remains & India (25% duty) remains on the backfoot compared with Japan (15% duty) on exports to US.

Valuation

▪ We model in higher volume growth of ~7% (earlier ~5%) & higher realizations from FY25-27E. Imposition of ADD should be a game changer as it will improve the margins & ROCE of the company. Concerns around weak export market & slower industry growth remains an overhang but is transitory once global demand picks up pace. Also, IS price has witnessed improvement by 25-30% from the bottom, stabilization of raw material prices, normalization of freight cost and strong FCF generation (FCF yield of 10-15%) are the positives.

▪ Currently, the stock is trading at P/E of ~10x on March 27E EPS of Rs 15.1. With imposition of ADD & stated positive triggers, we upgrade our target multiple to 15x (earlier 12x) and arrive at a target price of Rs 227 per share which offers upside of ~50% from current valuations, thereby maintaining our BUY rating on the stock.